Watch as Roger Philipp, CPA, CGMA, creates the mental framework to help you truly understand Audit Evidence and how to ensure these findings are sufficient and appropriate for the auditor's conclusions.

Tune in to learn:

• Where obtaining evidence fits into the overall flow of the audit

• The 4 levels of Audit Evidence

• Different types of substantive testing

• Helpful mnemonics for organizing and understanding information about Audit Evidence

Connect with us:

Website: https://accounting.uworld.com/cpa-rev...

Blog: https://accounting.uworld.com/blog/cp...

Twitter: / uworldrogercpa

Facebook: / uworldrogercpareview

Instagram: / uworldrogercpareview

Pinterest: / uworldrogercpareview

LinkedIn: / uworld-roger-cpa-review

Are you accounting faculty looking for FREE CPA Exam resources in the classroom? Visit our Professor Resource Center: https://accounting.uworld.com/cpa-rev...

Transcript Sneak Peek:

Welcome, welcome to the next section called Audit Evidence, Audit Evidence. Now, this is an important area because as we look at the audit, and at least here the steps in the audit process, let's come on over here.

We've talked about preparing for the audit, so that's getting ready, we talked about that in the first section. We're getting ready for the audit, we have to decide, are we gonna take the job? Do they have integrity? Am I properly trained? Am I proficient? Am I independent, clear mental attitude? Can I act with skill? Can I act with due diligence? Am I, as I said, independent?

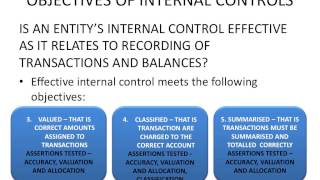

Then we said, okay, let's go up to obtaining and understanding. This was internal control, obtaining and understanding in internal control, assessing RMM, performing T of C, that was very heavily tested, that talks about understanding internal control, so we need to understand the design, document it, assess Control Risk, reassess, do your T of C, reassess, and then draw conclusions, document it.

We talked about internal control reports, different types, if it was in conjunction with the financial statement audit where you not give an opinion, versus statements on stance for attestation engagements where you're giving an opinion, versus PCOB audit where you're giving an opinion on both the internal control and the financial statements.

So we've gone through all that, we decided, "Hey, if reliance is high, great, I'll do less Substantive Testing, relia--" And we've been talking about that since day one, remember day one when you still cared about this exam? Are you excited about being a CPA?

We said, "Hey, if reliance is high that means Control Risk is low, or RMM is low, that means we're willing to let our acceptable level of Detection Risk go up, that means we'll do less Substantive Testing. Vice versa, if reliance is low Control Risk is high, Detection Risk's low, that means we're gonna do more Substantive."

Well, since day one we've been saying, reliance inverse relationship, if this goes up this goes down, if this goes down this goes up. So we've talked about reliance, that your T of C, that your ARCC and your RIIO, what are we testing for? Authorization, recording, custody, comparison.

Информация по комментариям в разработке