The following 21 sections summarize the amendments and compare them with prior provisions.

A. Summary of the Amendments

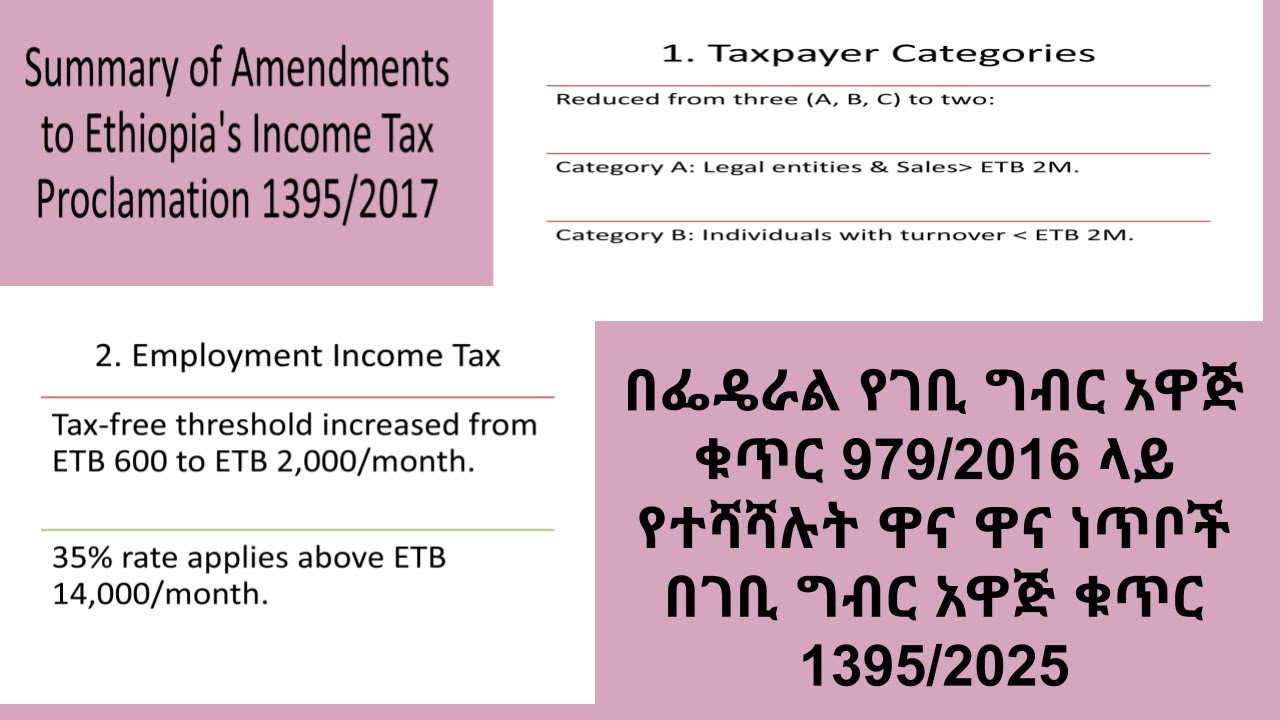

1. Taxpayer Categories Reduced

The previous three taxpayer categories have been consolidated into two:

• Category A: Applies to legal entities and anyone with annual turnover above ETB 2,000,000.

• Category B: Includes individuals (excluding legal entities) with annual turnover below ETB 2,000,000.

Previously, there was a third, “Category C,” which has now been removed.

2. Employment Income Tax Updates

The tax-free threshold for employment income has increased from ETB 600 to ETB 2,000 per month. The highest marginal tax rate of 35% now only applies to monthly earnings above ETB 14,000. These changes are effective from July 7, 2025.

3. Rental Income Tax Adjustments

Tax brackets for individual rental income have been raised, with higher thresholds. The progressive structure remains, but the brackets are more generous.

4. Business Income Tax for Individuals

Personal business income tax brackets have been aligned with the new employment and rental income brackets, ensuring consistency across personal income sources.

5. Presumptive Taxation for Category B Taxpayers

The lump-sum Turnover Tax (TOT) has been abolished. Now, businesses under Category B with turnover below ETB 2 million are taxed between 2% and 9% of their annual gross sales, as detailed in the new tax tables.

6. Corporate Income Tax

The corporate tax rate remains at 30%. However, the amendment introduces an advance payment requirement, explained below.

7. Advance Income Tax Payments

Both Category A and B taxpayers are now required to make quarterly advance payments:

• Category A: 25% of the prior year’s tax, paid within 5 days after each quarter.

• Category B: Same percentage, but within 15 days, starting Hamle 1 (July 8).

New taxpayers are exempt in their first year.

8. Minimum Alternate Tax

A minimum alternate tax of 2.5% on gross income applies if regular business income tax falls below this threshold. The minimum is calculated as:

• 2.5% of turnover for most businesses

• 2.5% of net banking income for banks

• 2.5% of gross premiums for insurance companies

• 2.5% of commission income for price-regulated companies

Credits may be claimed for up to five years. Presumptive taxpayers (Category B, under the turnover regime) are exempt from this tax.

9. Local Withholding Tax Increase

The local withholding tax rate has risen from 2% to 3%. The deduction threshold is now ETB 10,000 for services (up from ETB 3,000) and ETB 20,000 for goods (up from ETB 10,000).

10. Dividend Income Tax Increase

Withholding tax on dividends is now 15% (previously 10%). The tax is final and not subject to further assessment, except for dividends distributed within certain groups or to permanent establishments in Ethiopia. “Group of companies” refers to a controlling company holding over 50% of shares in other companies.

11. Undistributed Profit Tax Rate Increase

Tax on profits not distributed or reinvested within a year has increased from 10% to 15%.

12. Repatriated Profit Tax Rate Increase

Tax on profits transferred from a foreign branch to a head office outside Ethiopia has also increased from 10% to 15%.

13. Interest in Income Tax

Interest income is now subject to a 10% final withholding tax (up from 5%). This applies to residents and non-residents with a permanent establishment in Ethiopia. There are specific rules for financial institution deposits and credit-based interest.

14. Royalty Income Tax Rate Increase

Royalty payments to residents are taxed at 15% of the gross royalty, or 10% if related to art and culture. Non-residents are taxed at 15%. Previously, the rate was 5% for both groups.

15. Tax on Game Winnings

The tax on winnings from games of chance held in Ethiopia has increased from 15% to 25%, levied on the gross winnings.

16. Gains on Disposal of Investment Assets

Income tax on gains from selling immovable assets, shares, or bonds is set at 15%. The new calculation method allows for a 30% inflation adjustment. This excludes private residences held for at least two years.

17. Increased Nonresident Taxes

Rates for nonresidents are now:

• Insurance premium or royalty: 15% (was 5%)

• Dividend: 15% (was 10%)

• Interest: 15% (was 10%)

• Management/technical fee: 15% (unchanged)

18. Non-resident Entertainer Tax Increase

Tax on non-resident entertainers performing in Ethiopia has increased from 10% to 15%, calculated on gross income with no deductions.

19. Digital Content Creation Income

Income from digital content creation (YouTube, social media, podcasts, online sales) is now taxable. If considered business income, it is taxed at the standard rate; otherwise, a final 15% tax applies.

20. Digital Services Tax

A new tax of up to 5% may be levied on digital services (e.g., streaming, cloud computing) provided by foreign companies to Ethiopian consumers. The exact rate and implementation will be set by regulation.

21. Limits on Cash Transactions

Информация по комментариям в разработке