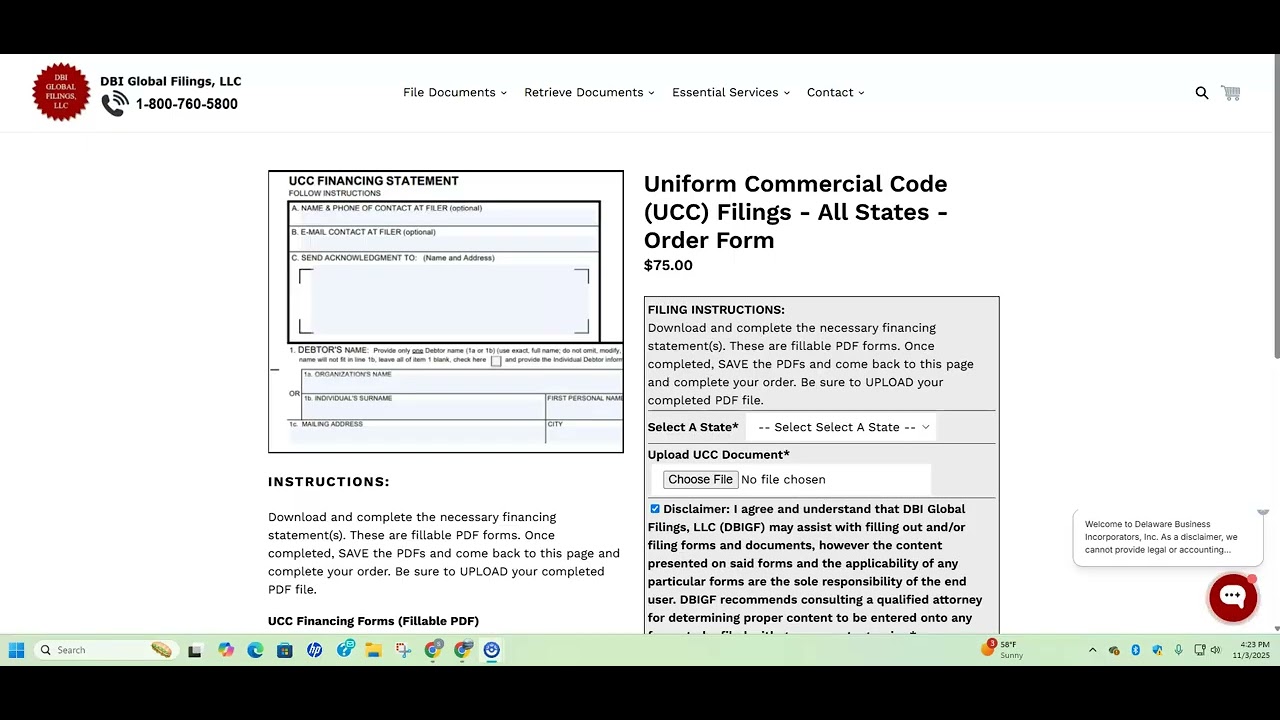

Click Here to Order Filings: https://dbiglobalfilings.com/products...

Click here to order searches: https://dbiglobalfilings.com/products...

What is a UCC-3 and Why Does it Matter?

________________________________________

Ever heard of a UCC-3 form? If you've ever taken out a business loan or used personal property as collateral, this little piece of paper is a critical part of the process. It's the form that manages the entire lifecycle of a loan, from start to finish.

Welcome to DBI GLOBAL FILINGS. I'm Russell Murray, and today, we're demystifying the UCC-3, or Uniform Commercial Code Amendment form. We'll cover what it is, why you need it, and the potential pitfalls of getting it wrong.

________________________________________

Imagine you pay off your business loan in full. You're free and clear, right? Well, not quite. The public record might still show an active lien on your assets, which can complicate future financing or sales.

That's where the UCC-3 comes in. It's the legal document used to update the public record and confirm that a security interest is no longer valid, or that details of the loan have changed.

________________________________________

Think of the UCC-1 as the beginning of a security agreement—it's the initial filing that gives public notice of a creditor's claim on collateral. The UCC-3 is the amendment form used to manage that initial statement over time. It's not a standalone document; it always refers back to an existing UCC-1 filing number.

There are four main types of UCC-3 filings:

1. Continuation: UCC-1 filings expire after five years. A UCC-3 continuation extends the life of the lien for another five years, ensuring the creditor's interest remains protected.

2. Termination: This is filed when the debt is fully satisfied and the secured party no longer has a claim on the collateral. It publicly releases the lien.

3. Party Amendment: This updates information, like if the debtor or secured party changes their name or address.

4. Collateral Amendment/Assignment: This can add or remove collateral from the agreement, or transfer the rights of the secured party to a new party, like when loans are sold between banks.

________________________________________

Filing a UCC-3 isn't just paperwork; it has significant legal consequences. Mistakes can be costly.

First, ensure you have the correct file number of the initial UCC-1. An incorrect number means your amendment might not apply to the intended record.

Timing is everything, especially with continuations. They must be filed within a specific six-month window before the original filing expires. Miss that deadline, and your lien lapses, potentially causing you to lose your priority claim to another creditor.

And be very careful with terminations. A mistaken or unauthorized termination, even if unintentional, can be considered effective in court and result in losing a billion-dollar security interest, as some major companies have learned the hard way.

________________________________________

The key takeaway? The UCC-3 is a powerful tool for maintaining accurate public records throughout the life of a secured transaction. Proper filing protects both debtors (by clearing their records) and secured parties (by maintaining their priority).

Because the rules can be intricate and vary slightly by state, it's always best practice to consult with a legal professional or a specialized filing service to ensure compliance.

Do you have more questions about UCC filings or commercial law? Let me know in the comments below!

Thank you for watching.

UCC-3, UCC3, UCC filing, UCC termination, UCC statement, UCC financing statement, Uniform Commercial Code, UCC lien, lien release, terminate UCC, how to terminate UCC, UCC-1 termination, UCC-3 form, legal, law, business law, business finance, finance, secured party, debtor, collateral, loan paid off, remove UCC lien, UCC search, legal forms, business guide, small business, legal education, debt, security interest, filing a UCC-3, UCC basics, commercial code.

Информация по комментариям в разработке