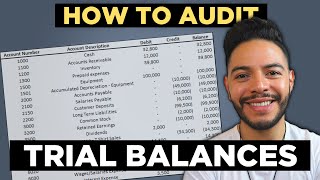

In this session, cover accounts receivable confirmations.

✔️Accounting students or CPA Exam candidates, check my website for additional resources: https://farhatlectures.com/

📧Connect with me on social media: https://linktr.ee/farhatlectures

#cpaexam #cpaexaminindia #professorfarhat

Positive Confirmation

A positive confirmation is a communication addressed to the debtor requesting the recipient to confirm directly whether the balance as stated on the confirmation request is correct or incorrect.

A blank confirmation form is a type of positive confirmation that does not state the amount on the confirmation but requests the recipient to fill in the balance or furnish other information. Because blank forms require the recipient to determine the information requested, they are considered more reliable than confirmations that include balance information. Blank forms are rarely used in practice because they often result in lower response rates.

Negative Confirmation

A negative confirmation is also addressed to the debtor but requests a response only when the debtor disagrees with the stated amount.

A positive confirmation is more reliable evidence because the auditor can perform follow-up procedures if a response is not received from the debtor. With a negative confirmation, failure to reply must be regarded as a correct response, even though the debtor may have ignored the confirmation request.

Offsetting the reliability disadvantage, negative confirmations are less expensive to send than positive confirmations, and thus more can be distributed for the same total cost. Negative confirmations cost less because there are no second requests and no follow-up of nonresponses.

The auditor has assessed the risk of material misstatement as low and has obtained sufficient appropriate evidence regarding the design and operating effectiveness of controls relevant to the assertion being tested by the confirmation procedure.

The population of items subject to negative confirmation procedures is made up of a large number of small, homogenous account balances, transactions, or other items.

The auditor expects a low exception rate.

The auditor reasonably believes that recipients of negative confirmation requests will give the requests adequate consideration. For example, if the response rate to positive confirmations in prior years was extremely high or if there are high response rates on audits of similar clients, it is likely that recipients will give negative confirmations reasonable consideration as well.

Negative confirmations are often used for audits of hospitals, retail stores, banks, and other industries in which the receivables are due from the general public. Auditors may use a combination of negative and positive confirmations by sending the latter to accounts with large balances and the former to those with small balances.

The auditor’s choice of confirmation falls along a continuum, starting with the use of no confirmations in some circumstances, to using only negatives, to using both negatives and positives, to using only positives. The primary factors affecting the auditor’s decision are the materiality of total accounts receivable, the number and size of individual accounts, control risk, inherent risk, the effectiveness of confirmations as audit evidence, and the availability of other audit evidence.

Timing

The most reliable evidence from confirmations is obtained when they are sent as close to the balance sheet date as possible. This permits the auditor to directly test the accounts receivable balance on the financial statements without making any inferences about the transactions taking place between the confirmation date and the balance sheet date. However, as a means of completing the audit on a timely basis, it is often necessary to confirm the accounts at an interim date. This is permissible if internal controls are adequate and can provide reasonable assurance that sales, cash receipts, and other credits are properly recorded between the date of the confirmation and the end of the accounting period. The auditor is likely to consider other factors in making the decision, including the materiality of accounts receivable and the auditor’s exposure to lawsuits because of the possibility of client bankruptcy and similar risks.

If the decision is made to confirm accounts receivable before year-end, the auditor typically prepares a roll-forward schedule that reconciles the accounts receivable balance at the confirmation date to accounts receivable at the balance sheet date. In addition to performing analytical procedures on the activity during the intervening period, it may be necessary to test the transactions occurring between the confirmation date and the balance sheet date.

Информация по комментариям в разработке